In a town like Mt Vernon, where hard work, common sense, and looking out for your neighbors still go a long way, money habits are often passed down just like family recipes. But some important financial ideas can get overlooked—and, over time, they quietly shape nearly every household… especially when it comes to credit and compound interest.

Compound interest is one of the most powerful forces in personal finance. Around here, it might not sound as important as a day’s work or keeping things paid on time, but it adds up in a big way. Used wisely, it can quietly help build savings over time. Ignored, it can just as quietly take thousands out of your pocket. The difference really comes down to knowing how it works—and making small, steady decisions that hold up over time.

This isn’t Wall Street talk or a fancy investment strategy. It’s everyday life—credit cards, car loans, mortgages, and savings—right here in Mt Vernon.

Compound interest is when interest starts earning interest—so the balance grows faster than most people expect.

At first, the impact feels small, but over time it accelerates and grows more noticeable. This difference is either helping them or hurting them.

It’s like rolling a snowball down a hill—it starts small, but it doesn’t stay that way.

When Interest Works Against You

Most people experience the downside of compound interest through debt, especially credit cards and long-term loans.

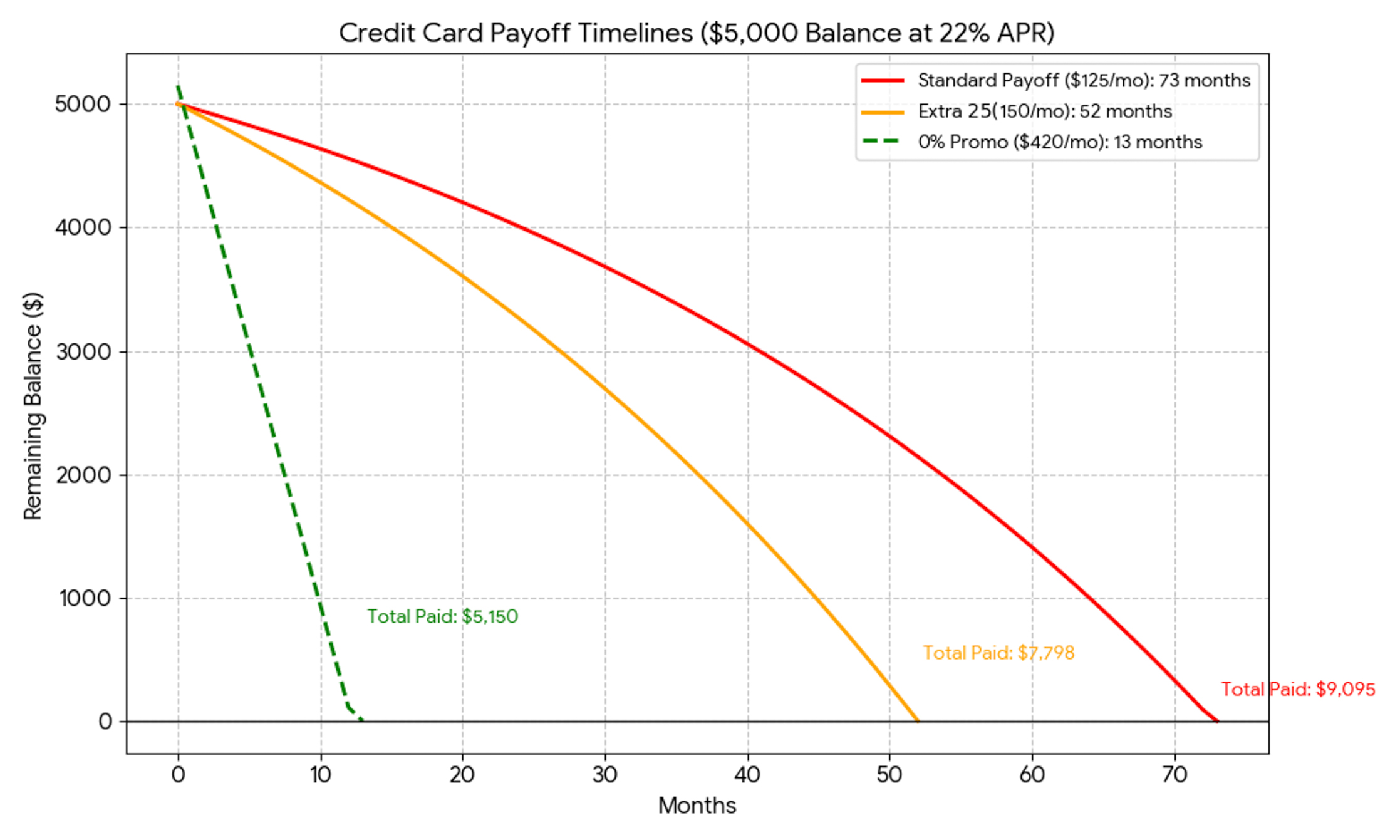

Let’s take a common situation. You carry a $5,000 balance on a credit card with a 22% interest rate. If you only make the minimum payment, interest is added each month—not just to the original balance, but to the new total.

Over time, that $5,000 can turn into $8,000 to $10,000 paid, depending on how long it takes to pay off.

This isn’t unusual. The kids need back-to-school clothing and supplies, and the ER visit costs more than expected. You tell yourself you’ll pay it off next month… But life doesn’t always cooperate. The balance sticks, and interest quietly keeps growing.

A Smarter Move: Using 0% Promotions

One way to stop that growth is to use a 0% promotional balance transfer card or a 0% promotional purchase credit card.

Here’s how that might look:

Move a $5,000 balance to a 0% interest card

Pay a 3% transfer fee ($150)

Get 12–18 months with no interest

If you pay about $420 per month, you could eliminate the balance within a year—saving thousands in interest. Using a 0% intro will simply avoid interest and fees altogether.

Even small increases above the minimum payment can make a meaningful difference. For example, if your minimum payment is $125 and you consistently pay just $150 instead—only $25 more—that extra amount goes directly toward reducing your balance faster. Over time, this reduces the amount of interest that can accumulate, shaving months (or even years) off your payoff timeline while saving hundreds or thousands of dollars.

That’s money that could have gone toward a used tractor, a kid’s first car, or just a little breathing room at the end of the month.

The Mortgage Most People Underestimate

Mortgages are often the biggest financial commitment a person makes, yet many people don’t realize how much interest they pay over time.

Consider this example:

$250,000 mortgage

6.5% interest rate

30-year term

The monthly payment is about $1,580. But over the life of the loan, you’ll pay roughly $320,000 or more in interest alone.

In other words, you’re buying the house, and another house's worth of interest.

Small Changes, Big Savings

Now here’s where things get interesting.

Add $100 extra each month:

Pay off the loan about 5–6 years early

Save approximately $60,000 to $75,000 in interest

Switch to biweekly payments:

Make half-payments every two weeks

This equals one extra full payment per year

Pay off the loan about 4–5 years early

Save approximately $50,000 to $65,000 in interest

Two neighbors move into the same street, with similar houses and jobs. One sticks with the standard payment. The other adds just a little extra each month.

Years later, one is still making payments. The other owns their home and keeps thousands of dollars that could be used for their kids' College Education.

The same principle that increases debt can also build wealth if used correctly.

If you invest $200 a month starting at age 25 and earn around 7% annually, you could end up with over $500,000 by retirement.

If you wait until age 35 to start, even if you contribute more each month, you’ll likely end up with significantly less.

The lesson is simple: time matters more than timing.

It’s not someone on TV doing this. It’s a teacher or a mechanic. A young couple in town, setting aside what they can… It’s not flashy, and it doesn’t feel like much at first. But over time, the growth builds momentum. This is the same snowball effect, but this time the snowball represents wealth and not debt.

A simple way to understand compound growth is the “Rule of 9.” At around an 8% return, your money can double approximately every nine years.

$10,000 becomes $20,000 in about 9 years

$20,000 becomes $40,000 in about 18 years

$40,000 becomes $80,000 in about 27 years

That growth comes from time and compounding, not additional contributions.

This is how many people quietly build wealth over time—not through big risks, but through consistency and patience.

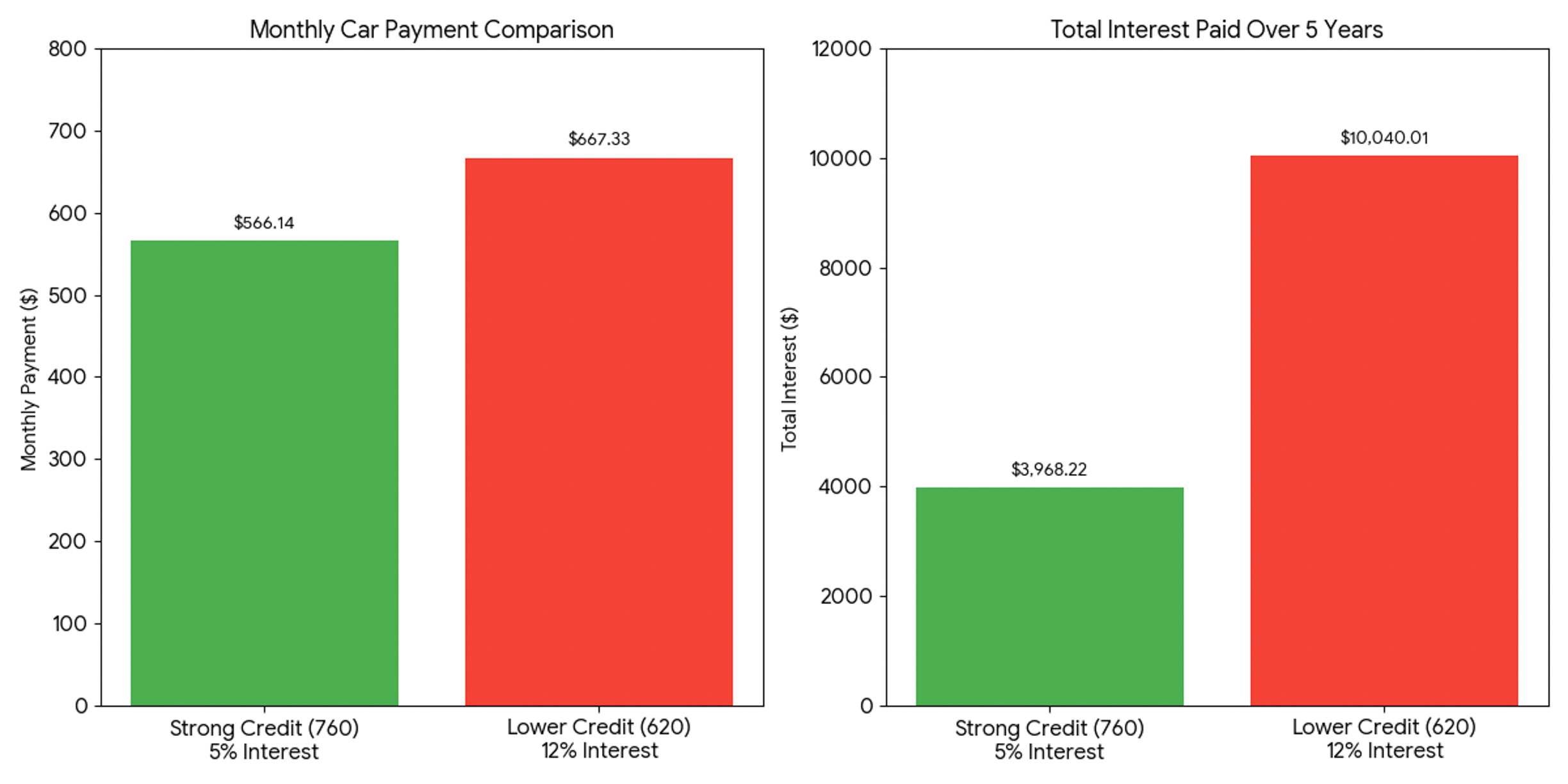

Your credit score plays a major role in whether compound interest helps you or hurts you—especially when borrowing.

Let’s compare two coworkers obtaining the same $30,000 car loan over five years:

Strong credit (around 760):

Interest rate: ~5%

Monthly payment: about $566

Total interest paid: around $4,000

Lower credit (around 620):

Interest rate: ~12%

Monthly payment: about $667

Total interest paid: around $10,000

That’s about $100 more per month and $6,000 more overall—for the same vehicle.

Over the life of multiple loans, that extra interest can add up to tens of thousands of dollars. Now imagine redirecting that same money into investments instead—where compound interest works for you as mentioned earlier.

Many people don’t realize that credit scores can also affect insurance rates.

Insurance companies often use a credit-based score to help determine auto and homeowners insurance premiums.

Around here, two folks can have the exact same driving record and still pay totally different insurance, just because of credit. Over time, that’s not a small change either… We're talking hundreds, sometimes thousands.

And if you’ve ever added a teen driver to your policy, you already know—insurance doesn’t just go up, it starts acting like it runs the place.

One simple way to help the next generation is by adding your child as an authorized user on a credit card.

When done responsibly, this can:

Help them build credit early

Improve their chances of qualifying for loans later

Teach real-world financial responsibility

The key is keeping things disciplined. Low balances and on-time payments matter most. Good habits build them up, but bad habits can set them back just as fast. In a small town where people look out for each other, it’s an easy way to pass down both trust and opportunity.

Beyond credit, parents can also teach the basics of compound interest and simple investing in a way kids actually understand. When they see how money can grow over time or shrink when misused, it sticks with them more than any textbook or lecture.

Show how compound interest builds wealth through saving and investing

Explain how debt can quietly grow if it’s not managed

Turn financial lessons into everyday, real-life examples

Even simple comparisons, like saving a few dollars versus carrying a card balance, can make it click.

And when you add in hands-on habits like budgeting, setting small savings goals, or trying out basic investing, kids start to see the bigger picture: credit isn’t just a score—it’s part of how long-term wealth is built.